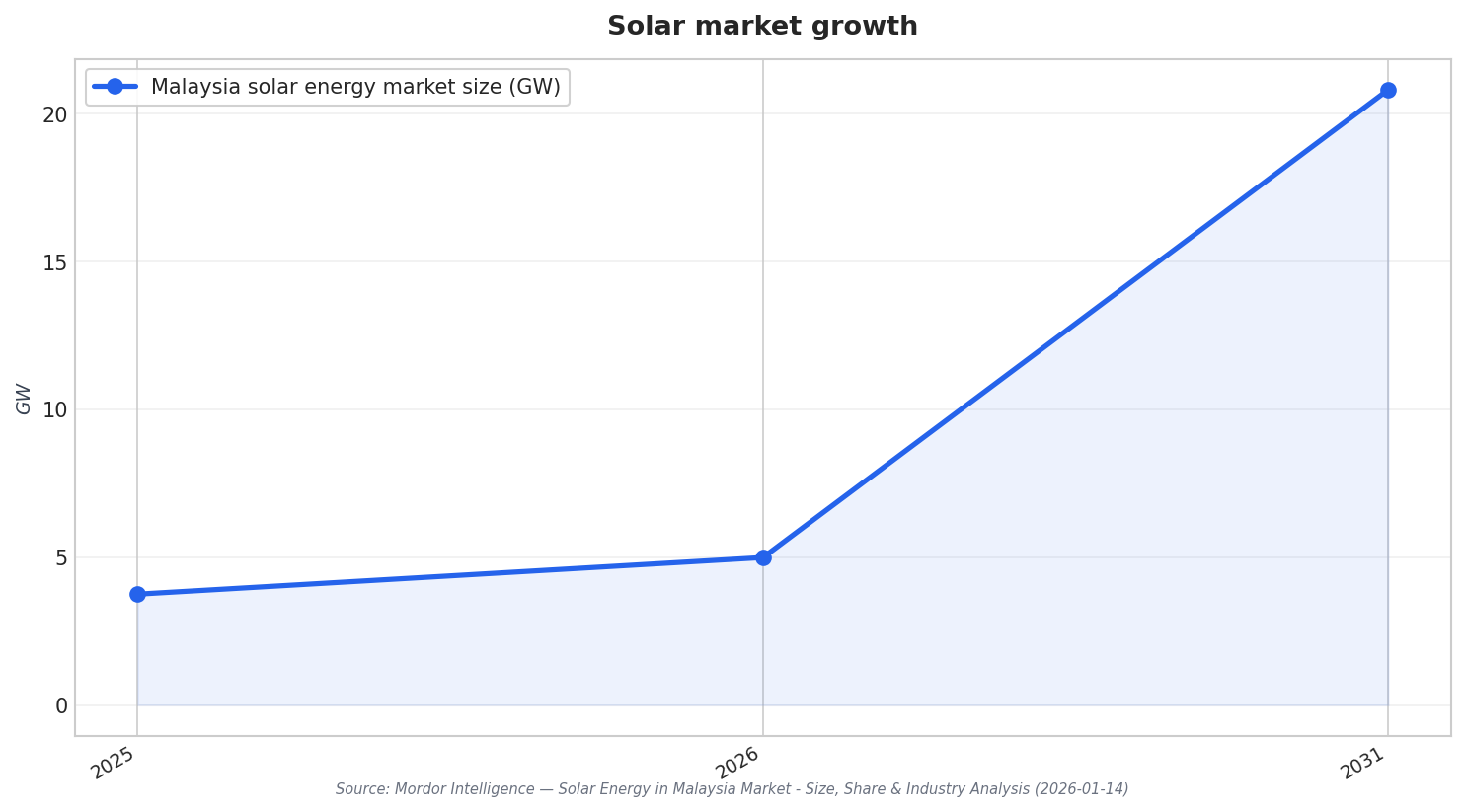

Malaysia’s solar momentum is increasingly visible in both utility-scale procurement and distributed rooftop adoption. According to Mordor Intelligence, the Malaysia Solar Energy Market is expected to grow from 3.75 GW in 2025 to 4.99 GW in 2026, and is forecast to reach 20.82 GW by 2031, at a 33.1% CAGR over 2026–2031. In the same 2025 snapshot, solar PV held 100.00% of market share by technology, while on-grid assets accounted for 91.42% of market size. This growth narrative is reinforced by government-led tenders, corporate renewable procurement, and demand linked to data center expansion in Johor and Selangor.

The Large Scale Solar (LSS) mechanism remains a central anchor because it standardizes offtake and pushes price discovery. Mordor Intelligence notes that LSS5 was awarded 2 GW in 2024 at an average tariff of RM0.1699 per kWh, and that LSS PETRA 5+ aims for another 2 GW in 2025. In parallel, Simply Wall St frames LSS5 as part of a long-term national strategy to reach 70% renewable energy installed capacity and carbon neutrality by 2050, while also citing a separate contract of approximately US$8.6 million for a 9.5 MW solar facility under the program. Together, these details show a tender pipeline that is both sizeable and continuous, with pricing pressure and clearer scheduling for developers.

LSS5+ Scale Meets Rooftop Reality

Project awards illustrate how LSS5+ is translating policy into concrete builds. SolarQuarter reports that Solarvest Holdings Berhad was appointed EPCC and technology partner for a RM1.06 billion LSS5+ project awarded by Malakoff Corporation Berhad’s subsidiary, Malakoff Silver Solar Sdn. Bhd. The facility is described as 690 MWp, located in Larut and Matang, Perak, spanning approximately 1,400 acres, and scheduled for commercial operation by the first quarter of 2028. Once operational, it is expected to generate up to 970,000 MWh annually and supply electricity to an estimated 230,000 households, stated as equivalent to around 2–3% of households in Malaysia. SolarQuarter also points to the role of smart grid technologies and BESS in supporting grid stability.

Rooftop solar, however, still shows a gap between technical potential and current adoption. TransitionZero estimates 1.75 GW of installed rooftop solar capacity nationwide, with 80% concentrated in Selangor, Johor, Kedah, and Pulau Pinang, and highlights an estimated 42 GW of technical potential. It also notes that Malaysia will launch the Solar Accelerated Transition Action Programme (Solar ATAP) on 1 January 2026, building on earlier Net Energy Metering (NEM) policy. BusinessToday adds a consumer-side perspective: across Malaysia’s 10.4 million retail electricity users, only 65,000 currently use rooftop solar, while a Community Renewable Energy Aggregation Mechanism (CREAM) expected in 2H 2025 would allow homeowners to lease rooftops for installations.

Solar acceleration also sits inside a broader grid-and-policy transition. Mordor Intelligence estimates Malaysia’s renewable energy market at 13.68 GW in 2026, growing from 11.09 GW in 2025, with projections of 39.03 GW by 2031 at a 23.33% CAGR for 2026–2031. NETR is described as setting targets of 31% renewable energy by 2025 and 40% by 2035, while Tenaga Nasional Berhad (TNB) is cited with a MYR 42.9 billion capex commitment, allocating 64% to grid reinforcement. The same source cites data-center investments of MYR 162 billion booked from 2021 to H1 2024, supporting corporate offtake pathways. Taken together, LSS scale, rooftop activation, and grid upgrades define the next phase of Malaysia’s energy transition.

How fast is Malaysia’s solar market expected to grow through 2031?

What did LSS5 award, and what was the average tariff?

What are the key details of Solarvest’s LSS5+ project in Perak?

How large is Malaysia’s current rooftop solar base, and where is it concentrated?

What do the latest forecasts imply for the Malaysia Solar Energy Market outlook?